Why I Bought Bitcoin Volatility When Nobody Wanted It

Introduction

Three weeks ago, I initiated a Bitcoin long strangle position.

At the time, there was no strong directional view behind the trade. I was not attempting to predict whether Bitcoin would rally or decline.

Instead, the opportunity came from the options market itself.

Implied volatility had fallen to levels that I considered unusually low relative to recent history, creating an attractive environment to own optionality.

Looking Beyond Direction

Most market participants focus on a single question:

Where will Bitcoin go next?

While direction matters, I often find it more useful to ask a different question:

Is volatility cheap or expensive?

Options allow investors to trade not only price, but also uncertainty.

When implied volatility becomes depressed, option premiums become relatively inexpensive. In such environments, a trader can potentially benefit from a significant move in either direction without needing to predict the direction itself.

This was the framework behind the trade.

The Market Environment

At the time of entry:

- Bitcoin price: 80k

- IV Percentile: 20

- Days to Expiration: 50

- Structure: Long Strangle

- Position Size: 2700 USD premium for 30 delta call and put

The market appeared calm.

Volatility expectations were low.

Many participants were focused on the absence of movement rather than the possibility that movement could return.

Historically, periods of compressed volatility are often followed by periods of expansion. While this is not guaranteed, the risk/reward profile was attractive enough to justify the position.

The Cost of Being Early

Owning volatility is rarely comfortable.

Unlike option sellers, long volatility positions pay for optionality through time decay.

Every day that the market remains inactive, option buyers face:

- Theta decay (my position has theta decay of 50 USD/day)

- Lower time value

- Potential mark-to-market losses (largest unrealized loss was 1600 USD)

For approximately 3 weeks, the trade experienced exactly this challenge.

The market moved less than expected.

The position drifted lower.

At times, it appeared that the thesis might not play out.

This is an important reminder that good trades and comfortable trades are often very different things.

When Volatility Returned

Eventually, market conditions changed.

A significant increase in uncertainty led to a sharp expansion in implied volatility.

As volatility expectations increased, option prices rose.

The position benefited from:

- Increased implied volatility.

- Larger realized market movements.

- Improved option valuations across the structure.

IV BEFORE VS AFTER

At entry, Bitcoin’s DVOL stood at 38.36, with an IV Rank of 9.5 and an IV Percentile of 20.8, indicating that implied volatility was trading near the lower end of its one-year range.

Following a period of market uncertainty, DVOL rose above 50, reaching a peak of approximately 82 before stabilizing. This repricing pushed IV Percentile above 50%, substantially increasing option valuations and benefiting long volatility positions.

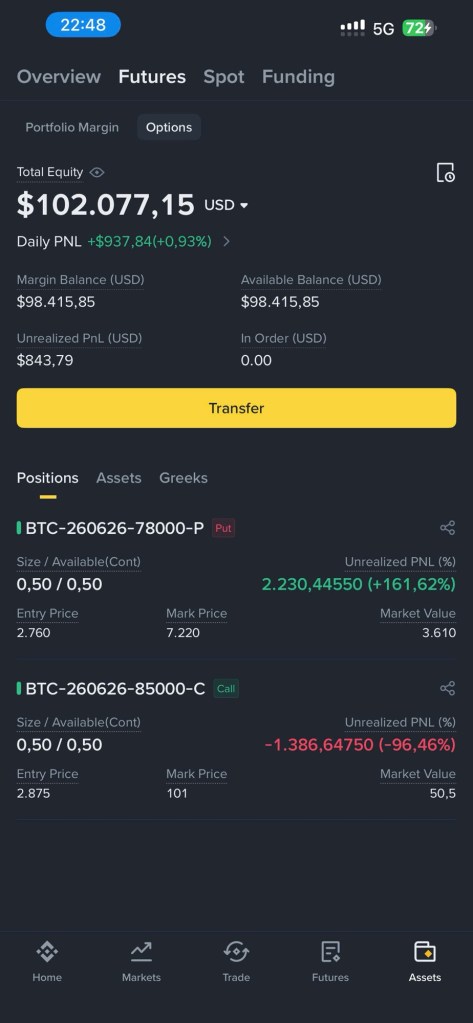

SCREENSHOT OF POSITION AFTER VOL EXPANSION

The trade ultimately generated approximately profit of about 1200 USD.

More importantly, it demonstrated the value of entering positions when the market is underpricing uncertainty.

Lessons From The Trade

1. Volatility Is An Asset Class

Many traders think only in terms of bullish or bearish outcomes.

Options provide another dimension.

Sometimes the opportunity is not in predicting direction, but in identifying mispriced volatility.

2. Cheap Optionality Can Be Valuable

When implied volatility becomes unusually low, the cost of being wrong decreases.

The market does not need to move in a specific direction.

It simply needs to move.

3. Patience Matters

Long volatility positions often require patience.

Theta decay can create pressure before the thesis has time to develop.

Position sizing and risk management become critical.

4. Regimes Change

The best opportunities are rarely permanent.

A successful trade often changes the environment that created it.

Current Positioning

Following the volatility expansion, the opportunity set has evolved.

The market is now pricing significantly more uncertainty than it did at the time of entry.

As a result, I have gradually shifted from being a buyer of volatility toward selectively selling option premium through short put positions.

The objective remains unchanged:

Identify situations where risk and reward become asymmetric and position accordingly.

[INSERT CURRENT PORTFOLIO SNAPSHOT]

Final Thoughts

This trade was not about forecasting Bitcoin.

It was about recognizing that volatility itself had become unusually inexpensive.

Markets constantly alternate between underpricing and overpricing risk.

My process focuses on identifying those shifts and adapting accordingly.

Sometimes that means owning volatility.

Sometimes it means selling it.

The key is understanding which side of the trade offers the more attractive risk/reward profile at a given point in time.

This article is provided for educational purposes only and should not be considered investment advice. Past performance does not guarantee future results.